The requested article has expired, and is no longer available. Any related articles, and user comments are shown below.

© (c) Copyright Thomson Reuters 2016.

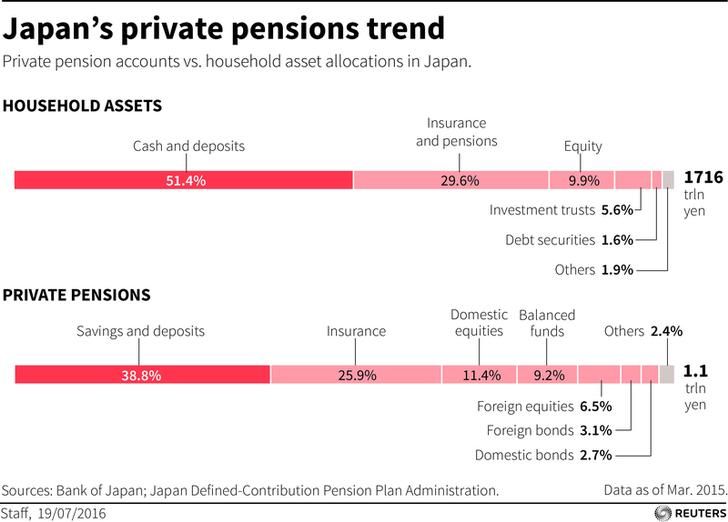

No retiree left behind: Japan turns to riskier DIY pensions

By Minami Funakoshi TOKYO©2024 GPlusMedia Inc.

28 Comments

Login to comment

kibousha

For those who are wondering, search google for "個人型DC" (kojin gata) if you want to know more about how to go about it in Japanese.

Yubaru

Based upon the current economy this is a given, yet there still needs to be a better system to adjust the money being paid out in pensions to people who have huge savings accounts. I know this has been discussed, and Abe will never go for it because it would mean his head.

Aly Rustom

Which begs the question why even bother to pay into the pension system? especially since most retirees have to get "silver" jobs just to make ends meet.

This is what happens when you don't have immigration. You reap what you sow. I worry so much about my son growing up here though..

GW

I think this is the key, govt is trying to draw in more suckers so they can then set up a possible REAL plan themselves, this will make setting yrself up for retirement harder for many!

Schopenhauer

From my investment experiences, it is very difficult to make profits on stocks. I would rather choose consumser tax at 25%.

Kokuzi

"invested half her money in foreign stocks and bonds and half in domestic stocks and bonds - she said she learned about diversifying her assets at a personal finance seminar." A.K.A. gambling. An amateur should not be buying individual stocks and bonds, leave that to billionaire investors like Carl Icahn. I know an older Japanese woman who has already lost 1/4 of her savings through buying individual stocks and bonds, but refuses to change her approach. You should at least buy ETFs (for example: https://www.blackrock.com/jp/ishares/ ) but there should be a range of fixed income, preferreds, equities, trust funds, etc for a balanced retirement portfolio.

fxgai

These folks in the article are misled. Don't they know that the government can print as much as it likes without risk of negative consequences, ever?

There's no risk!

FizzBit

My 2 cents...invest in anything "vintage Coleman"......

smithinjapan

"Only those who pay state pension fees are eligible to set up private pension accounts."

This is the fine print, peeps. They still want YOUR money to fund their gambles, for sure, but now they can quite literally say it is up to you to fund your own pension later, and if you didn't join these "DIY" schemes it's your own fault.

Can't expect them to do what they are supposed to, after all.

Duck70

Yes, GW! That's critical, you have to pay into the Ponzi first.

5SpeedRacer5

It is all fun and games until someone gets hurt.

I agree that the folks in the article are misled. But they are misled because I would bet none of them could read a financial statement or prospectus to save their life. And they will invest in FOREIGN stocks based on BLOGS. Right. That is going to work out really well. Two years ago the biggest securities company in Japan cold called me to get me to buy Turkish bonds. Sounds like a joke, but no. I am not joking. What they did was laughable. They were going to charge 3% of my investment up front to shield me from FX risk AND to cover exchange costs. So... they wanted to sell me a risky asset, but then have me pay to reduce the risk on it. I laughed at them and ridiculed them. I know few people able to spot that kind of "fraud" with confidence. Most people fall for that stuff all the time.

You know. People can do this saving for retirement stuff now anyway. If you don't think that public pensions, which you are legally obligated to contribute to, are going to support your post retirement lifestyle, then save more. Society is already meeting its obligation to you. If you want more, save more or invest more. Don't ask society for more. Why is this not obvious to people?

Oh, and one more thing: don't work at a job you hate. I suspect that is the real problem. Anyone looking forward to retirement every day is already dead. More money after retirement is not going to save your life today.

papigiulio

Easier said than done. 95% of the population doesn't know how to invest or a single thing about stocks. Wish a more saver way of saving would be available.

fxgai

Actually, I find some blogs do have insightful information. They need to be good if they want to keep readers to make money through the affiliate ads.

Yes, I'd put more faith in certain blogs than what securities companies might recommend, as they are just trying to drum up fee business.

Turkey was going through a coup attempt on the weekend and the top page of one broker website was peddling Turkish bonds too. Mind you, if you are going to buy them now might prove to be a better time to do so than 2 years ago (if you want to take the risk)

Robert Dykes

"almost all working-age Japanese to join private defined-contribution retirement plans"

Just not those of us working for a University (private and public) or public schools. Like 95% of us.

If I understand this article correctly, they are referring to the J-401k, which is not really like the IRA in the USA at all, it molded after the British system (sorry the name escapes me).

As of this year, koumuin still can not open a 401-k account, and this includes employees of private and public universities. If you are an American, there are a few other confusing caveats you need to look up yourself because I am far from an expert. But while J-citizens can invents in what ever they want, Americans will get double taxed if you invest in American held stocks and secruites so you have to stick to Japanese stocks (not a deal breaker but its best to diversify) and foreign held mutual and index funds are super heavily taxed for US citizens.

I think the law has already passed, but will not be enacted until sometime next year that will allow university employees to invest in a j-401k. But its still not that great Americans. If you have a j-souse, its probably best to open a NISA and/or J-401k in their name if you are an American. If you move back to the USA and get them a green card, things get complicated again as they are not under IRS/USA tax law like you.

kurisupisu

I bought a house outside Japan 12 years ago ;the price has risen by 10% , as I also rented it out! I'll bank the profits next year by selling it.

Simple!

Peter Qinghai

Back in the early 1980s, Chile reformed their pension system,

The masses didn't knoe squat about investing either; they quickly learned, and were the better for it.

The same goes for Jland.

Now's the time to be a CFP.

Wakarimasen

Govt. pension fund managers investing in riskier assets. what could possibly go wrong?

misunderstood

Do like the Chinese invest your hard armed money in foreign real estate

Disillusioned

It's hard to believe this can be true. How could they have made such a complete balls up of the pension system?

Will the people who decide to change to a private investment be able to transfer the money they have already paid into the national pension scam and/or will they still be entitled to receive payments on the amount they invested into the scam? I got scammed by the pension system for a few years and I'm wondering if I can transfer those funds into my private superannuation and retirement fund under these new laws.

Robert Dykes

"I bought a house outside Japan 12 years ago ;the price has risen by 10% , as I also rented it out! I'll bank the profits next year by selling it.

Simple!"

Simple? You are in the minority. Every homeowner I know in Japan has explained to me how much their house instantly depreciates.

Just heard a fellow professor say he lived in his house 7 of the last 20 years. Houses in Japan are financial death sentences for most. or unless you need the space, i could not imagine a worst "investment". In the USA unless you stay in one place for 5 years or longer, houses are no the investment they used to be.

The New York Times has an excellent calculator to determine if you should rent or buy. It has plenty of variables you can enter. I think most would be surprised that renting is often the more financially secure option.

http://www.nytimes.com/interactive/2014/upshot/buy-rent-calculator.html?_r=1

Ben Shearon

Check out RetireJapan.info for information in English about J401k, NISA, robo-advisors, etc.

I recommend saving at least 20% of your income for retirement.

inkochi

Retiring in Japan? Luckily I have alternatives. Yet, if it were Japan, I would start to look around for options less dependent on or independent of money. People will have less money here after retirement from now, so either get out or think outside the financial box. Yes, this includes alternative lifestyles, hippy-dom, but also less way-out things like cooperatives, migration to regional areas where some local governments are throwing houses and other things at people who will go. Switching to private pension and investment plans are simply orthodox versions of these except they are constructed around money.

Whatever happens, life for me is going to be seriously different later to what it is now. Lifestyle change is perhaps the only certainty, and it is only managing it now that gives me some kind of control

scoobydoo

You need more than a seminar to know how to make money in any market. Its take years to be good at what we do but people are mislead to believe they can make money with a little education. The pros know how to take the money out of the hands of the novice. Be warned

Jumin Rhee

If companies or guilds provided direct housing and basic food, even after retired, then there would be less strain. The need for a national pension would be reduced and could rely much more on savings and company pensions as there would be no housing or basic food costs.

kurisupisu

@Robert Dykes

The house purchased was not in Japan! Immigration and low interest rates with enhanced infrastructure spending was the reason for the average 10% year on year growth that I experienced.Part of my investment decision was based on immigration policies. Conversely, Japan with most of the wealth having been made by the previous generation seems not able to understand that without people and investment that there is only a downward spiral to look forward to......

Scrote

I don't really trust the providers of these pension plans. What are their charges and commissions? Are they betting against their customers in their own trades? I have read that simple indexed funds are better than managed funds as the fees should be much lower and they can often beat managed funds. These are not too popular with banks as there are fewer opportunities to rip off their customers.

I only own a small number of shares that I was given; every year the value seems to go down. It seems to me that if we assume that perpetual growth is impossible, companies will only be able to grow at the expense of one another. Unless you can pick the companies which have the potential to grow (you probably can't) investing in stocks is little better than gambling on roulette or the horses.

I am paying into the Japanese and UK state pension schemes. I should be able to combine two meagre pensions into one small one. I've thought about buying properties and becoming a money-grabbing landlord but I can't really be bothered with all the hassle. Instead, I've been putting some money into peer-to-peer loans. Time will tell if that pays off, or not.

Leigh Ivan Quintellio Wighton

This article is very misleading and vague. From what I can tell they are talking about the J401k. It is absolutely not a pension plan. It's a tax-free savings investment account that was modelled on the UK's ISA account. You can choose from a series of managed funds to invest up to something like 1.2 million yen a year in, and your gains are tax free, but for only 5 years. The UK ISA system has better yearly limits and I think the tax free gains are unlimited whereas the Japanese version is only good for 5 years. In any case, it's not a pension plan and you don't have the option to stop paying the national pension plan and just do this.